Rene, age 39, is a framing carpenter at a company that builds doors and windows. He has group disability insurance equivalent to 60% of his annual salary, which is $70,000. His monthly living expenses are $3,500. Since he has no pension plan at work, Rene has enrolled in an individual RRSP through payroll deductions ($1,000 per month). His RRSP savings currently amount to $45,000. In addition, Rene has $10,000 in a non-registered savings account. What should Rene’s life insurance agent advise him?

Wesley is a self-employed plumber. He meets with a licensed life insurance agent to explore his options regarding disability insurance. Wesley’s earnings have been stable over the past few years.His business generates gross income of $120,000 annually and write-off expenses of $30,000. Wesley’s average income tax rate is 30%. What income amount should be used to calculate the maximum disability benefits Wesley is entitled to?

Bachir owns a successful video game business and has 10 employees. The time has come to plan business succession and the eventual sale of the business. Bachir’s nephew Kharim, who shows a real interest in the business, is identified as his successor. Bachir would like to protect his sales price until such time as the business is sold to Kharim, who does not have the funds yet and will need a few years to amass the required amount. Bachir and Kharim consult insurance agent Bianca for advice. What should Bianca propose?

Kimeni meets with Orion, an insurance agent, to purchase segregated funds. After assessing Kimeni's needs, Orion suggests an index segregated fund. Kimeni agrees to invest $5,000 in the fund now and $200 every month.

With relation to this transaction, which of the following options is CORRECT about the Fund Facts document?

Planet Source decides to implement a defined contribution pension plan (DCPP) for its 75 employees. The company's president appoints Josie, the human resources director, as the plan administrator.

Which of the following BEST describes Josie's responsibility as a plan administrator?

Enzo meets with his insurance agent Theo to discuss his investment needs. When Theo asks Enzo about his liabilities, Enzo tells him that he purchased a house for $750,000 four years ago and his current mortgage balance is $600,000. He has a fixed interest rate on the mortgage of 3.5% for 5 years.

Which of the following statements about his mortgage is TRUE?

Karine receives $200,000 from her mother's estate and decides to purchase an annuity. Her insurance agent Serge goes over her options with her, and she chooses the annuity that best suits her needs. Serge proceeds with the transaction.

Which of the following statements about the transaction is TRUE?

Jessica is 61 years old and has $460,000 invested in a registered retirement savings plan (RRSP). She is retiring due to health issues that are expected to reduce her life expectancy and will prevent her from working until she is 65. She would like to transfer her RRSP funds into an annuity that will pay her monthly benefits for the rest of her life.

Which of the following annuities is the BEST option for her to purchase?

Caleb meets with Miles, his insurance agent, to invest for his retirement. Caleb tells Miles that he will not need his funds for the next 25 years, he is comfortable with market fluctuations, and he would like a fund that mimics the S&P/TSX Composite index.

Which of the following funds will best suit Caleb's needs?

Remi owns a registered annuity contract that pays him a $2,500 monthly benefit. He purchased the contract five years ago from money he accumulated in his registered pension plan. At the time, he named his wife Annette as the revocable beneficiary of the contract. Today, he calls Louisa, his insurance agent, to designate his sister as beneficiary of the contract instead. Louisa tells him that there are restrictions on the contract and that he cannot change the beneficiary designation.

Why is Remi unable to make the change?

Thien is 56 years old and has recently been diagnosed by his doctor with a heart condition for which there is no known treatment, and which has dramatically reduced his life expectancy. Thien has decided to take early retirement. Fortunately, after 30 years of service working as a credit officer at a local bank, he has accumulated a large sum in his pension plan. Thien's wife supports his decision to retire early. She is 49 and in good health, and plans to continue working and earning a lucrative income at her current position as a divorce lawyer at a prestigious law firm, at least until she reaches 65 years of age.

What type of annuity would BEST suit Thien's needs?

Hana, a 25-year-old personal assistant, recently got a job where the employer offers all employees access to a defined contribution pension plan (DCPP). Hana meets with the groupinsurance agent, Tom, because she must choose her investments and she doesn't know what she should choose. She is not very knowledgeable about investments, but since the money will only be used at retirement, she wants to invest in a fund that combines stocks and bonds and that is easy to understand.

Which fund should Tom suggest?

Aadi is retiring from Scotia Grand, his employer of 25 years. While employed, Aadi benefitted from the company's deferred profit sharing plan (DPSP) and over the years, he accumulated $75,000.

Where should Aadi transfer these funds on a tax-deferral basis, now that he is retired?

Luisa owns a balanced segregated fund currently valued at $50,000. Her mother Linda is the current revocable beneficiary of the policy. However, Luisa has been dating Benjamin for a year and would like to name him as the new beneficiary of her policy.

Which of the following statements about modifying the beneficiary designation is CORRECT?

Sebastian is a 44-year-old sales representative employed at Premier Aqua. He wants to take a year off to travel and relax. He has worked for the company for 25 years and accumulated $230,000 in adeferred profit sharing plan (DPSP). He would like to know if he can use some of the funds in his DPSP to fund his sabbatical.

Seven years ago, Amber invested $150,000 in a non-registered equity segregated fund. Her investment grew, and today, the market value of her fund is $165,000. She places an order to redeem her fund and she wants to know how her investment will be taxed.

Naomie meets with her new client, Keisha, to review her investment portfolio. Keisha is a 43-year-old sales representative who has been with Belmont Inc., a large pharmaceutical company, for 15 years. She earns a generous salary, plus bonuses. She also has a group tax-free savings account (TFSA) and a defined contribution pension plan (DCPP), all of which are invested in Belmont common shares.

What main need does Naomie have to address regarding Keisha’s investments?

Ontario residents, Juan and Maria, are a married couple approaching retirement. They have askedtheir representative Carlow to review the details of Maria’s defined benefit plan (DBPP).

Which of the following statements about Maria’s pension is CORRECT?

Jackson, a new life insurance agent, is planning to promote a group insurance plan to small businesses in the area. After some research, he is able to locate a list of small business contact information online. The list contains office hours, phone numbers, as well as the office addresses. He prints off the list and prepares marketing material pertaining to group insurance and mails it to each of the small businesses. Jackson’s business plan is to call the businesses one by one 14 days after the marketing material has been mailed. What should Jackson be aware of to comply with the usual business solicitation practice?

When Tim and Patricia were common-law spouses, they met with an insurance agent, Aelia, to purchase life insurance policies of $100,000 each, naming each other as beneficiaries of their policies. Five years later, Patricia leaves Tim to be with her personal trainer, Thomas. A year later, Patricia and Thomas marry, and Patricia gives birth to their baby, Cedrick. Tragically, just before Cedrick's 12th birthday, Patricia dies in a fiery car crash. She never modified her beneficiary designation.

Shortly after the crash, Thomas calls Aelia to inform her that Patricia has died and that he wants to claim the death benefit on her life insurance policy.

Who will receive the $100,000 death benefit?

Last month, Suzanne purchased a life insurance policy from a local agent. The agent told her that the policy would accrue a cash value that she could draw from in her retirement years and that the premium would never increase. After recently meeting with a close friend, who is a retired insurance advisor, she was dismayed to learn that what was sold to her is in fact a term policy with no cash value. If Suzanne wishes to make a formal complaint against the agent, which authority can assist her in doing so?

David, a respected career life insurance agent in his city, has a lot of older clients because he has been selling insurance for 35 years. One such senior, Craig Wilson, is 79 years old with a $150,000 universal life policy that he purchased in his 40s. Craig has several medical issues and may not live too much longer. Craig wants to create a bucket list in his final days but he has no savings to do the things he wants. So he contacts David to see if there is someone who can give him $50,000 now in exchange for the $150,000 insurance payout at his death. David knows a wealthy businessman who would purchase this policy as Craig wishes. What practice is David engaging in?

Dale meets with his last appointment of a busy workday. He is helping his client Larry fill out a disability insurance claim form. Larry suffered a heart attack a week ago and is at home recuperating. Larry will be unable to work for the next 6 months and needs the benefits as soon as possible to cover his expenses. The at-home appointment takes a little longer than scheduled and Dale finds himself rushing to his son’s big hockey tournament. In his haste, he puts Larry’s form in his briefcase and subsequently forgets to submit the form. Which responsibility did Dale breach?

Mike and Todd are both agents with Superior Insurance Company. Every Friday, they have lunch together at the local pub. One Friday, Mike forgets his wallet, so Todd pays both bills. Mike has a sales appointment that afternoon, where he will be signing a small term life insurance policy on a child. He decides to simply indicate that Todd is the agent of record so that Todd gets the compensation for the sale—an easy way to pay him back for lunch! What practice is Mike engaging in?

Edward and Shirley initiated a whole life insurance application for their daughter Christine when she was 15 years of age. As Christine was a student with limited income at the time, the agent set Edward and Shirley jointly as owning and paying the premiums of this policy. Edward was designated beneficiary. Who is the policyholder?

Mordecai's life insurance lapsed four years after the policy was issued because he failed to make premium payments. The insurer reinstated the policy several months later when he made the required payments and provided the medical and financial information the insurer required. Twelve months later, Mordecai commits suicide and his beneficiaries ask Larry, his insurance agent, whether the claim will be paid. What should Larry tell the beneficiaries?

Arianna has been an insurance agent with Ideal Life for over 15 years, always working hard to grow her client base and keep her existing clients happy. Last week, she prepared an elaborate insurance plan for Raphael, a potential new client. But when they meet, Raphael tells her he wants a second opinion. Arianna tells him that she cannot allow him to show or discuss details of her work with a potential competitor. She explains it's wrong for another agent to benefit from her work and knowledge.

Which of the following standards of conduct did Arianna contravene?

Emeka, a new insurance agent with Sunrise Insurance, meets with her client, Mosi. After analyzing Mosi's needs, Emeka determines that Mosi's current life insurance coverage with Starlight Insurance is more than sufficient. Nevertheless, she persuades Mosi to cancel his existing coverage and buy a new life insurance policy with Sunrise Insurance. She believes this is a good compromise because Mosi will have the coverage he needs, and the new transaction will pay her a commission. Which of the following offences did Emeka commit?

Danny purchases a $1,000,000 whole life insurance policy. He names his three daughters, Donna-Joe, Stephanie, and Michelle, as revocable beneficiaries with each receiving one-third of the death benefit.

If Michelle predeceases Danny, and Danny did not have a chance to modify his beneficiary designation, how will Danny’s death benefit be paid out?

Miguel applied for a disability insurance policy nearly three months ago. He recently received notice from his agent that his application was approved, with an exclusion applicable to his lower back due to a prior injury. The agent brought the exclusion amendment with the policy at the delivery appointment. Miguel signed and accepted it. He gave the agent a copy of a void cheque to set up direct billing for the premiums, but asked that they wait three days to draw the first premium, to coincide with his payday. The insurer drew the premium three days later, as requested. When did Miguel's policy take effect?

Mercedes is a single mother to her 5-year-old son Arthur. Arthur's father Richard is not in his son's life because he is a recovering drug dealer who spent the last 4 years in and out of prison. Mercedes has full custody of Arthur and cannot count on help from her family because they live in another province.

Wanting to ensure his well-being, in the event of her death, Mercedes purchases a $100,000 life insurance policy and names Arthur the sole beneficiary of the policy.

If she died without a will who would receive the death benefit?

Maeve is an Ontario resident. Fifteen years ago, she purchased a $250,000 whole life insurance policy and named her husband Guillaume as the primary beneficiary and her 4-year-old son Edwin as the contingent beneficiary. Last week, Tasha, Maeve's insurance agent called her to ask if she has had any life changes that would warrant a meeting to review her insurance coverage. Maeve informs her that over the last year she divorced Guillaume and that she is now living with her new boyfriend Eduardo. Tasha asks to meet Maeve to review her beneficiary designation. Who will receive Maeve's death benefit if she dies today?

Konrad is the owner of CrossBoy, a manufacturing company employing over 50 employees. Konrad recently took out a $500,000 loan to expand his business. Terrence works as a sales manager and is responsible for roughly 40% of the company’s revenue. Konrad recognizes the importance of Terrence's contributions to the success of the company. Therefore, in addition to a sizeable basesalary, CrossBoy also pays Terrence regular performance-based bonuses. Konrad understands that if Terrence dies prematurely, CrossBoy would suffer financially. What should he do to protect his company?

Goran and Tanja married two years ago. Last year, they purchased and moved into a three-bedroom house in the suburbs. The current balance on their mortgage is $655,000. They meet with Ljubomir, an insurance agent, to purchase a joint term life insurance policy to cover the mortgage. When Ljubomir asks about their existing coverage, Goran shares that he has none. Tanja explains that she owns a universal life (UL) policy with a level death benefit of $50,000 and a cash surrender value (CSV) of $5,000, purchased 6 years ago from another agent. Tanja would like to surrender her UL policy and use the $5,000 CSV to pay for a trip to Europe. What additional information about Tanja's UL policy does Ljubomir need to collect?

Alana, Meaghan, and Beatrice are equal shareholders of Advanced Tech Inc. They each own 100 shares of the company. Each share is currently worth $5,000. They recently signed a cross-purchase buy-sell agreement that is funded by life insurance. What will happen under this agreement if Alanadies today?

Edna is a 62-year-old widow living in Quebec. She meets with Yolanda, her insurance agent. Ednaworked part-time her whole life as a seamstress and has no savings. Her husband Donald had been working as a greeter at the local box store until his death 2 months ago at the age of 67. Since his passing, Edna has been struggling financially. She would like to know which of the following organizations will immediately pay her a benefit?

Aari and Jonila are a married couple in their late sixties. They both enjoy a comfortable retirement. Both receive regular payments from their pension plans, Old Age Security (OAS) and Canada Pension Plan (CPP). They own a house and a cottage that are both mortgage-free. They also have over $500,000 in savings and investments. They know that if one of them dies, the surviving spouse will be financially comfortable. The couple has two grown children to whom they would like to leave all their assets when they die. The couple informs Herbert, their insurance agent, that they want to make sure when they die that their children have the funds needed to pay the taxes on the assets that they will bequeath them.

Which life insurance policy would be most suited to meet the couple's needs?

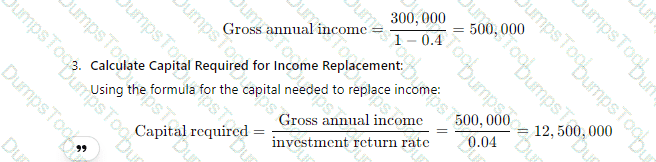

Oliver, an insurance agent, meets with Roman and Julie. They are a married couple with a five-year-old son William. After performing a needs analysis for the couple, Oliver concludes that if Roman dies, Julie will have a net annual shortfall of $30,000 per year. Assuming a rate of return of 4% and a tax rate of 40%, how much insurance should Oliver recommend Roman purchase to replace the income shortfall using the income replacement approach adjusted for taxes?

Jasper owns TeleVida, a successful production company with over 50 employees. He wants to expand the company by opening an office in another province. Jasper needs to take out a $500,000 20-year loan to make this expansion happen. However, he wants to make sure that if he dies while there’s an outstanding balance on the loan, the balance will be paid in full by the insurance company.

Francis owns a $250,000 insurance policy with an accidental death and dismemberment (AD&D) rider. Francis calls his insurance agent Andrew to inform him that he permanently lost the use of his right hand. He explains to Andrew that his brother shot him when he broke into his brother’s house to recover a gold watch that was rightfully his. Francis wants to know how much he will receive from his AD&D rider.

Jasper is the sole breadwinner in his family. His wife Stephanie has chosen to dedicate all of her time to raising their 3 young children. Luckily, Jasper earns a monthly after-tax income of $25,000 working as a family doctor in the local clinic. Jasper meets with his insurance agent Odda to purchase a life insurance policy that will ensure his family will be able to continue to enjoy their current lifestyle in the event of his death. If his average tax rate is 40% and theinvestment return is 4%, how much life insurance should Jasper purchase based on the income replacement approach?

Aaliyah is a 37-year-old account manager at a large pharmaceutical company. She earns $300,000 a year plus bonuses. She meets with Theo, an insurance agent, to review her life insurance needs. Theo deduces that Aaliyah needs a $250,000 universal life (UL) insurance policy. Aaliyah agrees but states that she wants to keep her premiums low. Which of the following UL death benefit options would BEST suit her needs?

Axel owns a $150,000 whole life insurance policy with an accumulated cash surrender value (CSV) of $20,000. His monthly premiums are $300, due on the fifth day of each month. Axel misses his November 5 premium payment and then dies a few weeks later, on November 20.

Germain is a life insurance agent. This morning, he receives a call from Jason, whose wife, Rosalie owned a $50,000 life insurance policy that she purchased from Germain seven years ago. Jason explains that Rosalie had a heart attack and died last week. Germain promises to help as much as he can.

Maxine meets with Toshiko, an insurance agent for United Life, to purchase a $10 million universal life insurance policy. Once United Life reviews Maxine's file, they agree to insure her for $3 million. United Life then contacts Extra Life Company, who agrees to insure Maxine for the additional $7 million. Toshiko asks his supervisor Bob how the death benefit will be paid to Maxine's beneficiary when she dies.

Justin decides to lease the personal vehicle of his friend Simon, who owns a window installation company. They agree on Justin having exclusive use of the vehicle in exchange for some renovations on Simon's house. What type of contract is this?

Kirill purchases a $250,000 permanent life insurance policy on the life of his grandson, Dmitry. Kirill asks his wife Katya to pay the policy premiums and names his daughter, Natalya, as the subrogated policyholder. He does not name a beneficiary. Subsequently, Kirill dies without a will.

Who will become the new policyholder?

Vasu, an insurance agent, meets with Francine, his new client. Francine wants to purchase a disability insurance policy. Vasu helps her complete the application form. In the process, he collects all the required medical and lifestyle information on his client and wonders what he must do with the information he collected.

Which of the following options is CORRECT?

Nathalie worked for 25 years as an administrative assistant at a manufacturing company. When she left the company 10 years ago, she transferred the money that she accumulated from the company’s pension plan into a locked-in retirement account (LIRA). Now she is 60 years of age and would like to withdraw the money from the LIRA.

Under which of the following circumstances would Nathalie be allowed to withdraw her funds?

Julie and Jim have been married for 16 years and decide to divorce. They draw up a list of property that will be partitioned based on the provisions of family patrimony: the family home, the cars, the RRSPs, and the benefits accrued with the RRQ during the marriage. What other items should be added to Julie and Jim's list?

Alexandre, a financial security advisor, recently left FinCode Inc. because of an unresolved dispute with the company. He is continuing his career as an independent advisor. This week, he has an appointment with a client who tells him that he met with another FinCode Inc. employee. However, that employee has a disciplinary record at the CSF for fraudulently copying a signature on a form. Since the client does not work in insurance and the information is public knowledge, Alexandre provides him with some clarification regarding the other advisor’s case. How can Alexandre encourage the client to do business with him without denigrating his competitor?

Isaac and Natasha, Quebec residents, were married 18 years ago. At the time, they visited a notary to get married under the "separation as to property" matrimonial regime and had indicated their wish to waive the application of the division of the patrimony by agreement. After experiencing a series of personal crises, the couple is now divorcing.

Which of the following assets, if any, will they have to separate when they divorce?

Insurance of persons advisor Somalia is careful to comply with the standards and regulations when she meets with potential clients. Under no circumstances would she want them to feel aggrieved or not respected. She makes sure to know their rights. Which legislation does Somalia not have to worry about?

Jean, who is in business, would like to understand why his segregated funds, which resemble mutual funds, allow this type of asset to be sheltered from creditors. How should Patrice, his financial security advisor, answer?

Last week, at a dinner party, Dario, an insurance agent, met Andrew, a successful businessperson with a net worth of over $10 million. Dario spent the evening following Andrew around, telling him how he could help him manage his finances. The day after the meeting, Dario sent a fruit basket to Andrew's office. Every day since, Dario has been calling and urging Andrew to meet with him and take advantage of his services and insurance products.

Which duties and obligations did Dario break?

Claudie’s mother has been the policyholder and beneficiary of an insurance policy on the life of Claudie since she was five years of age. Claudie is now the mother of a three-month-old boy. Claudie would like for Marc-André, her de facto spouse, to be the beneficiary of the policy. What steps need to be taken in order for this to happen?

Alexandre has just become a father. He wishes to take out a life insurance policy from Antoine, an insurance of persons representative. During their meeting, Alexandre mentions his love of mountain climbing. What should Antoine do?

Adèle retired a few months ago. She sold some of her assets and would like to use the funds to take out a term annuity to increase her retirement income. Adèle brings a $300,000 cheque to Germain, her financial security advisor, and wants to begin receiving lifetime guaranteedbenefits in one month with the right to use capital in the event of an emergency. When Germain tells her about alienating capital, the capitalization phase, and the payment phase, Adèle becomes confused and asks for clearer explanations. What can Germain say to help Adèle understand?

The company Xtra is growing. Mr. Trenet, chair of the executive committee, invites his financial security advisor, Noah, to meet with them to underwrite an annuity contract. The treasurer of Xtra offers to invest $2,500,000 of the company’s retained earnings. Before voting on a resolution to designate a policyholder, the treasurer asks Noah if Xtra can be designated as the policyholder instead of Mr. Trenet. What answer should Noah give?

Pierre-Marc, aged 32, is a dentist with a rich clientele. His income is substantial. Five years ago, he purchased an “any occupation” disability insurance policy. Today he meets with Joseph, his life insurance agent, to determine whether this type of coverage is still adequate. What should Joseph tell him?

Harper owns a disability insurance policy that will pay her a monthly benefit if she becomes unable to work. At the time she applied for the policy, Harper was a new graduate with an annual income of $60,000, and she qualified for a monthly benefit of $3,000. Instead of taking the maximum benefit, she focused on paying off her student loans and keeping her insurance premiums low. She elected to purchase a monthly benefit of $2,500 and add the future purchase option (FPO) rider for up to $500 a month of additional coverage. Now she is further along in her career, Harper earns $100,000 a year, and she meets with her insurance agent Trish to increase her coverage. Harper would like her new monthly benefit to be $5,000.

Which of the following statements about Harper’s coverage is TRUE?

On June 5, Karl completed an application for critical illness coverage and paid an annual premiumof $1,250. On June 25, the underwriter approved the policy under standard conditions and sent it to the agent, who received it on July 7. The agent contacted the client on August 8 and the date for delivery was set at August 10. On August 12, Karl learns that he will lose his job at the end of the month. As such, he decides to cancel the policy, returning it to the insurer on August 15. What is the rule governing Karl’s right to have his premium refunded?

Larry, an insurance agent, meets with Ethan, a freelance photographer, to review his insurance needs. Larry tells Ethan that he wants to collect all pertinent financial information to prepare a net worth statement for Ethan.

Why does Larry want to prepare Ethan’s net worth statement?

TESTED 27 Apr 2025

A black and white math equation Description automatically generated with medium confidence

A black and white math equation Description automatically generated with medium confidence A number with numbers and lines Description automatically generated with medium confidence

A number with numbers and lines Description automatically generated with medium confidence A close-up of a math Description automatically generated

A close-up of a math Description automatically generated